Ornstein Uhlenbeck Proces

A quantitative research and visualization framework for analyzing complex options strategies, payoff structures, and volatility dynamics.

Problem & Motivation

Options strategies are inherently non-linear and difficult to reason about without proper visualization. Retail tools oversimplify payoff structures, while professional systems are often opaque or inaccessible. This project aims to provide a transparent, extensible, and mathematically grounded framework for understanding options behavior under different market conditions.

System Architecture

Technical Implementation

- Python-based modular architecture

- NumPy & Pandas for numerical computation

- Payoff surface generation and strategy composition

- Matplotlib for publication-quality visualization

- Designed for extensibility toward stochastic modeling

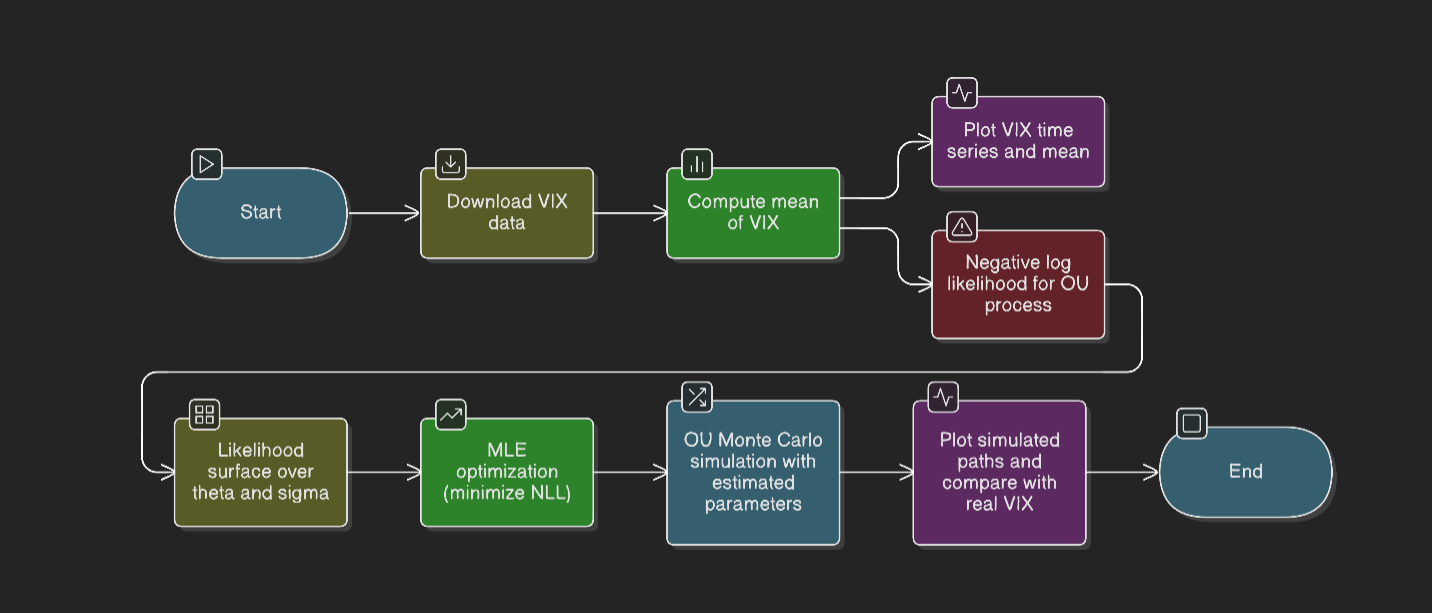

Research Extension: Volatility Modeling

The framework is extended with stochastic modeling of volatility using mean-reverting processes such as the Ornstein–Uhlenbeck model, applied to instruments like the VIX. Parameter estimation is performed via maximum likelihood, followed by Monte Carlo simulation for forward scenario analysis.

Full mathematical derivation and code are available as a separate research document.